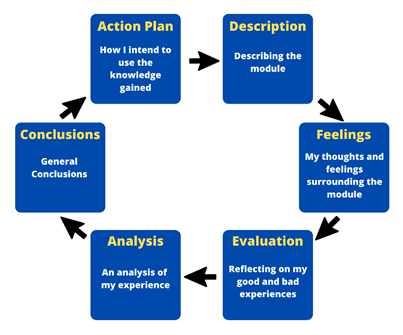

After a stimulating eleven weeks of digital submersion, all whilst challenging any perceptions of learning I previously had, the BEMM129 Digital Business Models course has sadly come to an end. This blog will see me critically reflect on my experience using Gibbs’ (1988) reflective model.

Gibbs’ reflective model (1988). Created with Canva

Description

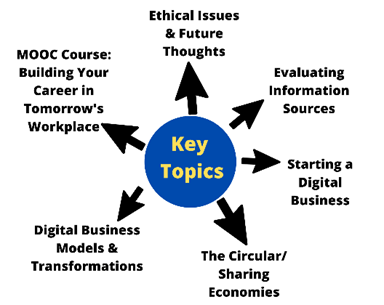

BEMM129 has been a module like no other. Located entirely online, I felt that this module had two key objectives:

To inform on how digital innovations are revolutionising the world we live in.

To help students feel more confident in a digital environment.

Created with Canva

This course has seen me write two blogs, one on the changing role of the retail banker and the other on Monzo. I have also thoroughly enjoyed reading the work of my peers and giving my thoughts on their blogs, all whilst contributing to the weekly discussion topics:

My main feeling entering this module was apprehension. I had never labelled myself as being particularly imaginative, a quality which I had associated with digital success. This was clear in the early topics where I was reluctant to post any comments.

As the weeks progressed, my confidence grew, and I found myself participating more and more in discussions. I feel like a lot of this came from seeing my peers interacting with each other, which definitely pushed me to interact more with the module content.

Evaluationand Analysis

The best experience from this module for me has been discovering a new learning style known as connectivism (Siemens, 2005), a social learning process based upon the connections through digital avenues (e.g. blogs, comments, MOOC, ELE and other trusted online sources).

Dr George Siemens discussing connectivism

The use of blogs as the format of assessment made the learning experience more enjoyable. This opened my eyes to a more expressive style of writing and forced me to step outside my comfort zone.

I felt I struggled with the more creative side to the module, such as when creating graphics. I felt like this limited the scope of my blogs and was compounded by only having the free version of WordPress.

I felt that throughout the module I used a good mix of original and additional sources, however sometimes I was reluctant to give my own thoughts without any evidence, which is an area I still need to work on.

Created with Canva

Conclusion

My experience on BEMM129 has been incredibly insightful and enjoyable. I now feel like I am more comfortable in a digital environment and I intend to continue this journey.

Action Plan

Word count: 414

References

Gibbs, G. (1988). Learning by doing:A guide to teaching and learning methods. Oxford: Further Education Unit, Oxford Polytechnic.

Siemens, G. (2005). Connectivism: a learning theory for the digital age. International Journal of Instructional Technology and Distance Learning, 2(1), 3-10.

Monzo’s ‘hot coral’ card has received much applause

For far too long, banking has been harder than it needs to be. From pesky hidden fees and charges to the stress of managing your accounts, the days of traditional banking methods are outnumbered. The opportunity for a newcomer to disrupt the norms had presented itself. An opportunity that Monzo has seized with both hands.

Their mission? To make money work for everyone. Their product? A banking hub that lives entirely on your phone. Their customer base two years ago? 500,000. Their customer base now? Almost 4 million.

Founded in 2015, Monzo is a UK-based challenger bank making real strives in the industry. I opened my account roughly one year ago and haven’t looked back since. There are a number of attractive features, from the absence of fees when exchanging foreign currencies to the sheer simplicity with which I can manage my money. All of these features are underpinned by one glowing factor: Monzo’s ability to leverage digital technologies.

Is it actually a bank?

Technically, yes. Monzo obtained their full UK banking license in 2017. But practically speaking, they operate nothing like a traditional bank. They are a ‘challenger bank’, operating in the margin between an online current/savings account and a financial planner, a new breed of technology-driven and customer-centric institutions (Burnmark, 2016).

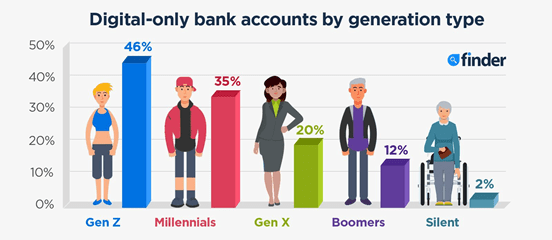

The rising popularity of challenger banks has been driven primarily by Gen Z and Millennials, with one in three Millennials stating that their primary banking relationship is with a challenger bank (Kearney, 2020).

The driving force behind Monzo’s success is the decision to be completely digital. Face-to-face interaction has always been a pivotal part of the traditional banking service, however as outlined in my previous blog, times are changing.

Going completely digital and leveraging the digital technologies at their disposal has resulted in numerous efficiency-increasing and cost-reduction opportunities. These opportunities have presented themselves in two key areas: automation of services and the migration of front-end activity to digital channels, such as via the implementation of machine-learning and artificial intelligence, which has reduced the requirement for a large customer service team.

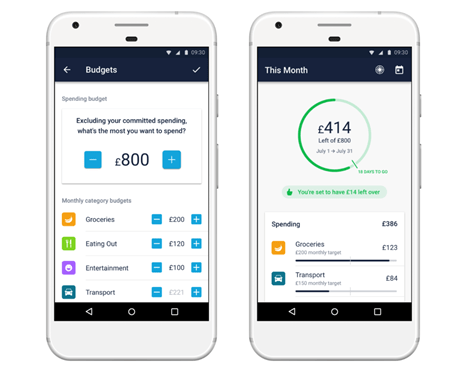

Artificial intelligence is used at Monzo to constantly look for opportunities to improve user experience, an area in which Monzo place a huge emphasis. The Monzo app is a perfect demonstration of this. From this hub, a number of slick features are available. Unlike most banks, your balance is instantly updated, and you receive a notification when you spend, making it easier to track balances. The easy-to-use budgeting tool and option to temporarily freeze your card gives you the ability to complete traditionally laborious tasks at the tap of a button. These user experiences are incomparable and barely scratch the surface of what Monzo offers.

Chief Executive Tom Blomfield suggests that banking behemoths such as HSBC and Barclays are crippled with outdated technology and principally focus on their existing set of financial products (CNBC, 2020). Traditional banks have certainly been slow to adopt the call from the banking community for greater digital features.

In contrast, Monzo has embraced this change which has paid dividends. Until recently, every customer resulted in a loss due to services free overseas cash withdrawals. However, in their 2019 annual report, it was detailed how the annual per-customer contribution margin is now a £4 profit (Monzo, 2020).

Unrivalled customer experience

From day one, customer centricity and transparency have been heralded as two key areas of focus for Monzo. A democratic culture has been established at the company, and Monzo have used their online presence to encourage customers to share suggestions and engage with the company via its blog and social media accounts. The Monzo community has therefore been involved with numerous important decisions, such as deciding the pricing method for ATM fees abroad (Monzo, 2017) and even providing name suggestions when Monzo had to legally change their name from Mondo (Monzo, 2016).

This hasn’t gone unnoticed by the customers. Monzo have set up a number of crowdfunds in recent years to raise crucial funds, where the community have given back for the faith that Monzo place in their users. Monzo also achieved a customer score of 82% in Which’s ‘best bank for 2020’ survey, trumping the scores at any high street bank (Which?, 2019).

Sustainable banking

As a start-up, innovation and evolution are crucial for success, especially in a crowded market where Monzo are competing not only with traditional banks, but also other challenger banks. Monzo recently transitioned from an outsourced faster payments gateway to an in-house faster payments connection, meaning that 100% of their technology is now hosted in-house. This is indicative of the innovative culture at Monzo.

Monzo’s ultimate goal is to become a sustainable, all-encompassing financial storefront which removes the hassle of routine financial chores. Current features being explored include being able to check your credit score and further development of tools for dealing with your salary, all of which are set to revolutionize the banking sector. Blomfield certainly has impressive plans for the company, and if the success of the last five years is anything to go by, exciting times lie ahead.

Like the majority of people in the UK, I use banking services every day. Whether this be using my credit card, transferring money to a friend after a night out or extending my overdraft (can you tell I’m a student?) the services provided by banks are a fundamental part of my life. Retail bankers play a key role in these front-end services, and it’s likely that all of us at some point have called on the expertise of these individuals to assist with our banking enquiries.

Yet as I sit here, I cannot recall the last time I went to a bank and acquired these services. So how can I be so reliant on these services traditionally provided by retail bankers, yet rarely have to speak to one? The answer lies in the evolution of the digital economy and technologies such as artificial intelligence (AI).

AI is the ability of machines, computer programmes and systems to perform the intellectual and creative functions of a person (Shabbir and Anwer, 2015), and is become increasingly prevalent in front end banking, from fraud detection and credit scoring to chatbots and voice assistants. The video below contains a number of high-profile individuals within the banking and financial services industry talking about the exciting possibilities of AI (Internet of Business, 2017).

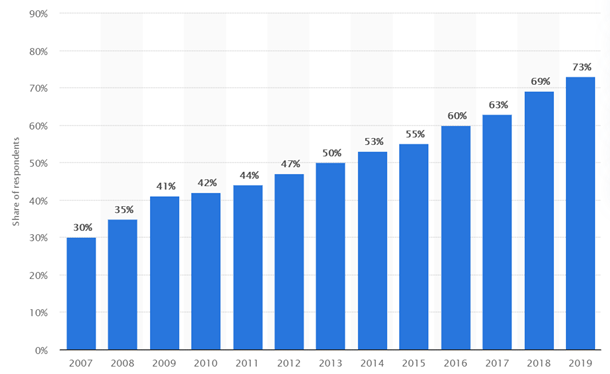

Another huge innovation in banking over the past decade has been the rise of online banking. The scope of features available via online banking is incredible, from simply transferring money to applying for a mortgage, with its evolution seemingly exponential. According to a recent survey, a staggering 73% of individuals in Great Britain regularly used online banking services in 2019, up from 42% in 2010 (Statista, 2020).

Online banking users in Great Britain from 2007 to 2019

The Economist Intelligence Unit report that coping with new technology is a top concern of retail bankers (EIU, 2019), and with these technology-based solutions replacing many branch-specific functions, it prompts the question: do these digital technologies represent a risk to the role of a retail banker?

The View from the Inside

To explore how these digital technologies have changed the role of a retail banker, I spoke to Niall Dewson of NatWest in Bridport. The message was clear: the fundamentals of the job haven’t changed, however the way in which this work is conducted has.

‘A customer may walk in to open a savings account and we help them do it on the app within 5 minutes, or 30 years ago a customer may have come in to make a large withdrawal of cash to pay someone and we would have talked about the benefits of paying by cheque, but now we would show them how to do this online’ says Niall. ‘Digital technologies allow us to streamline the traditional retail banking processes’ he adds.

AI in the form of chatbots has also had a big streamlining effect. The high demands of customer service have long been an issue for retail bankers, so the ability of chatbots to immediately answer questions and give sound financial advice without the customer ever having to speak to another human has helped to relieve some of this strain.

Niall stressed that the time saved due to digital technologies allows for more time to be invested into other responsibilities, such as having more in-depth conversations with those customers most in need of guidance, or undertaking further qualifications such as the personal banker accreditation. Increased popularity of digital technologies has also created new responsibilities for retail bankers due to new threats to customers in the form of hackers and scammers. Retail bankers are now being trained to provide advice for such threats in ‘community banking’ roles, suggesting a switch from a sales-based role to a service-based role.

Looking to the Future

It seems inevitable that the future of retail banking will become increasingly non face-to-face as customers demand the convenience of being able to do what they want, wherever they are, so long as the technology allows for it.

Some reports suggest that US banks could cut more than 200,000 jobs in the next decade (Financial Times, 2019), a worrying prediction for any retail banker. However, these digital technologies could also offer a potential opportunity for the transformation of roles in retail banking.

Pop-Up Branch

As banks continue to close their most uneconomic branches, we will likely see a trend towards pop-up and mobile-led banking hubs replacing traditional branches. Retail bankers will have to become more mobile, more technology-savvy and have greater knowledge about all of a bank’s products and services.

Niall tells me that banks have already started to offer more career and training opportunities which focus on developing the skills required to thrive in roles which leverage digital technologies, where specialist knowledge is augmented by digital technologies to provide an optimal service to customers.

The biggest factor which will ultimately decide the future for retail bankers is what the ceiling is for these digital technologies (if there is one), and how long will it take to reach this point. One thing is for certain- the digital revolution has reached banking and is showing no sign of slowing down.

Hi, my name is Ellis and I’m on the MSc International Management Course. I am from Somerset, near Glastonbury Festival, and decided to choose this module to gain a deeper understanding of how digital technologies are shaping the business world.